Loan Risk Reporting and Expected Loss

Mosaic utilizes a forward-looking expected loss model to provide

transparency and insight for risk management, due diligence, and CECL preparation

Dive into your portfolio with Mosaic

Make proactive decisions. Focus on growth. Increase earning potential.

What do we do?

Drive ahead of the curve with loan-level Expected Loss

Transform your data into useful information. Gain actionable intelligence.

-

Trending & Migrations

In addition to reporting and risk, Mosaic is a data repository that stores your loan data over time for powerful reporting.

-

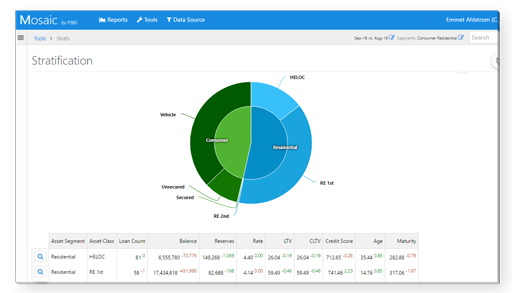

Portfolio Monitoring

Monitor your portfolio, identify concentration risk, stay on top of collateral values, and perform multi-dimensional portfolio analysis.

-

Report on what matters to you

Identify production characteristics by different focuses including branch and loan officer production.

-

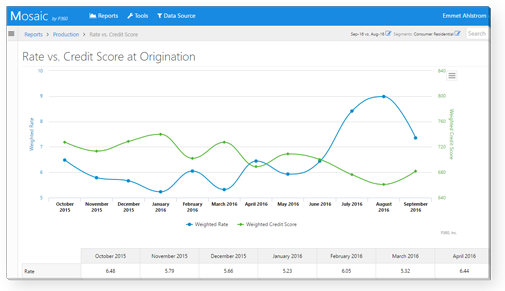

Monitor Rate and Risk

Monitor production to stay on top of your lending and profitability goals. Find out how your production is shaping your loan portfolio.

-

CECL Modeling

Mosaic manages CECL requirements and provides multiple economic scenarios so that lenders have sufficient data to model their own estimated losses.

-

Loan Level Risk

Including Risk Grades, Probability of Default, Loss Severity, Expected Loss (ALLL), and risk reporting.